Updated: Aug 6, 2020

‘Sustainable Investing’ as a term is incredibly broad (Krosinky and Robins, 2012; Gerrard, 2015; Mclean, 2015), and fluid. Over time, different organisations have applied their own individual meanings. And so the definition, type of assets and mental concept have all evolved (Kemper and Ballentine 2019) … into one big mess. And nothing really seems to be changing.

‘One woman’s “ethical investing” is another man’s “socially responsible investing”, and one firm’s “responsible investing” is another manager’s “sustainable investing”. – Krosinky and Robins, (2012)

Over the past decades, Sustainable Investing has become loaded with a myriad of meanings and definitions, until it doesn’t really have a meaning at all. Like a vague corporate buzzword. You’d expect a guy called “Chad” to talk about it while he encourages you to, “Think outside of the box” or some other BS bingo.

Confusingly, Sustainable Investing is also used interchangeably with other terms. Yikes. Krosinky and Robins highlight this ‘embarrassing richness of semantics’, in their book, stressing that ‘social’, ‘ethical’, ‘green’, ‘responsible’, ‘socially responsible’ and ‘sustainable’ are used synonymously across the investment industry. So while some investment firms use these words like a thesaurus, others apply really stringent (made up) meanings. Trying to compare the investment style in a conversation between a few of these managers is like trying to untangle spaghetti mixed with glue. Not worth the hassle.

The Forum for Sustainable and Responsible Investment (US SIF) add yet more terms to the mix including, ‘community investing’, ‘mission-related investing’ and ‘values-based investing’. The variety of definitions continue. Some academics perceive Sustainable Investing as integrating ‘certain kinds of non-financial concerns – variously called ethical, social, environmental or corporate governance criteria – in the otherwise strictly financials-driven investment process’ (Sandberg et al 2008, in Paetzold and Busch, 2014). Which is probably one of the loosest definitions out there … practically tearing down the floodgates for green washing.

A growing focus on returns

But there is some consensus building, managers are agreeing with the second half of the definition, “Investing”.

Back before 2015, when people watched DVDs and an iPhone was really something impressive, Sustainable Investing was generally seen as a kind of charitable “nice to have”. It wasn’t really viewed as “investing”. Definitions showed a trend of separation between Sustainable Investing and the ‘strictly financial’. Or in other words, it was like donating to charity. Nice, not essential. The phrase, “Investors who do good, but not well”, began cropping up (Junkus and Berry, 2015). I wonder if it still lingers around fusty wealth offices today.

Over time, that separation narrowed. After 2015, investors began to take Sustainable Investing more seriously. In today’s investment landscape, it’s widely accepted that this kind of investing can generate financial returns. Sure, there are some sceptics. Sustainable Investing hasn’t really had a long history to prove itself yet. And of course, it’s so open to interpretation that greenwashing can dilute the results. A lot. But there’s growing consensus that this (whatever it is!) is a revenue-driving approach.

This shift has changed the definition. Recent definitions tend to emphasise the financial benefits.

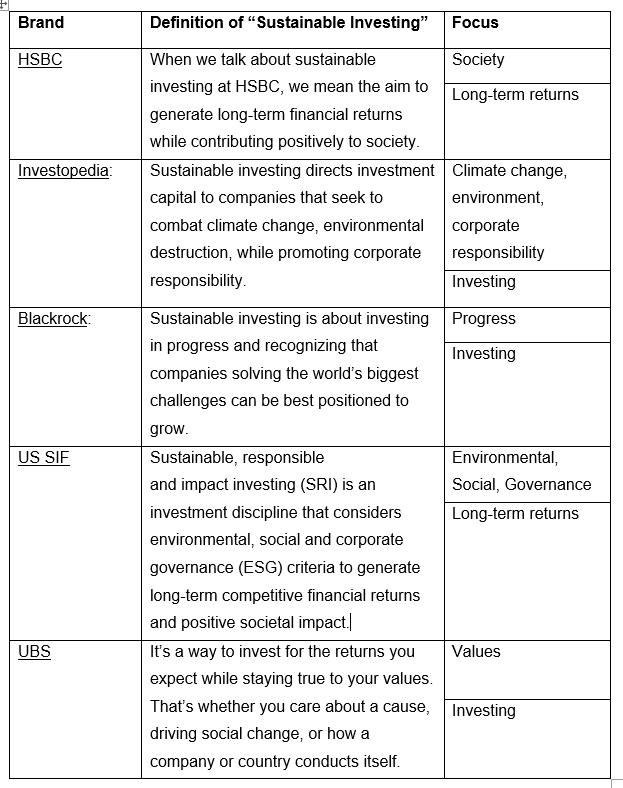

To highlight this, I’ve collected the first five definitions of Sustainable Investing on Google. As you can see, they’re all consistent when it comes to the financial side. They all talk about long-term returns or investing. But when it comes to the sticky issue of Sustainability, they freestyle. There’s no standardised definition, so managers have a lot of wiggle room to interpret the phrase how they like. Which is good for them, not so good for well-meaning investors.

Responsible Investing is not the same as Sustainable Investing, Sustainable Investing is not the same as ESG investing… but they’re all used interchangeably by institutions anyway. Gah.

One of the terms which seems to most mixed with Sustainable Investing, is SRI.

Confusingly, for the most part in Europe this refers to ‘Socially responsible investments’ whereas in North America it stands for ‘Sustainable responsible impact’. Fortunately, despite this, they seem to have identical meanings (Haigh and Hazleton, 2004, in Chang et al 2013, US SIF 2015, Eurosif 2016).

According to Garrison and Sanburg (2018), SRI describes negative screening, or exclusions. And Sustainable Investing describes investments with environmental focus. So this would make Sustainable Investing different from ESG investing, where the environment is just one third of the focus.

But what does it matter because they’re all used interchangeably anyway?

Even the Global Sustainable Investment Alliance uses SI and SRI interchangeably.

The GSIA uses an inclusive definition of sustainable investing, without drawing distinctions between this and related terms such as responsible investing or socially responsible investing. – Global Sustainable Investment Alliance, 2018.

Great.

So, what’s the impact of multiple definitions for investors?

Academics, governments, asset managers and more have all created their own meanings for the term. Brilliant. Nobody is speaking the same language. We have the SDG goals fighting one corner and the ESG principles (based on 2004 Darmstadt Sustainable Investment definitions) in the other. But they’re supposed to be on the same team. We have index funds deciding what sustainability means TO THEM, and filling green indices with oil, tobacco and sugary drinks. What we have, is basically a meaningless mess.

With this in mind, perhaps some of the impressive figures over past years – such as the 34% increase in SI between 2016 until January 2018 leading to a $30.7 trillion in sustainable assets under management or AUM (Global Sustainable Investment Alliance 2019) – should be taken with a pinch of salt.

Highlighting this, Mittelman (2018) points out that managers use this very broad term to describe a multitude of investments. If the term were to be refined or narrowed, would these statistics paint a different picture? The GSIA points out the managed Sustainable Investments’ market share dropped in Europe by 4% during 2018, following ‘stricter standards and definitions’, which supports this hypothesis.

More so, on a darker note, is it possible that the term is deliberately kept vague so that asset managers meet their targets and maintain a good public image?

With increasingly common mistrust for financial institutions (Park and Ghauri, 2013, Mclean 2015) especially after the 2008 crisis (Sackler 2017, White 2018), managers will need to work overtime to prove that they take Sustainable Investing seriously. With perceived complexity (Oxford Risk, 2019) being another key deterrent for sustainable clients, having no clear standard definition is good for neither clients nor the planet.