Updated: Apr 7, 2020

A little planning now can make a huge difference to your retirement income later. Getting a private pension pot while you are young is pain-free and extremely valuable for later in life.

I know, I know. It feels boring and far away. But the earlier you start planning, the more comfortable your retirement will be. It’s because of an economic rule called ‘compounding’. Every decade you can add to your pension timeline should multiply the amount of money in your retirement pot. To illustrate this point, I’ve used Nutmeg’s pension calculator.

Starting early

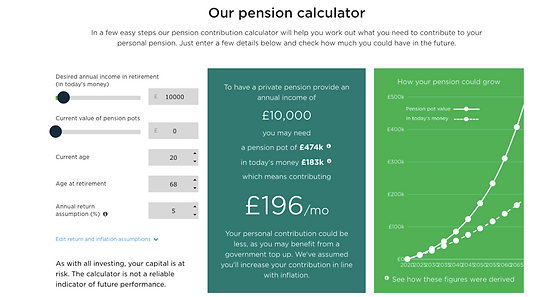

If you want to have an annual retirement income of £10,000 a year, you’ll need to be paying in £196 a month if you start when you’re 20.

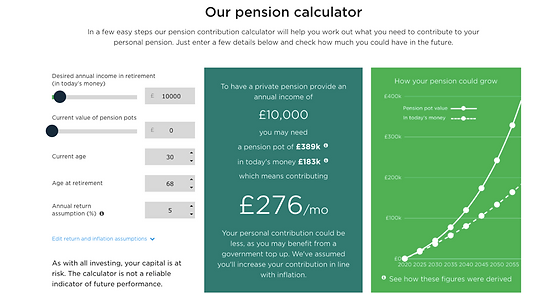

If you start when you’re 30, you’ll need to pay £276 per month.

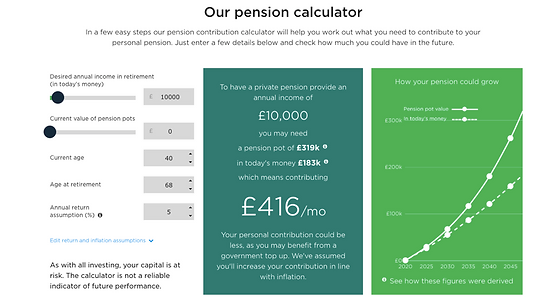

At 40 years old, you’ll need to be paying £416 per month.

Why do I need a private pension?

You’ll probably have a workplace pension, and a state pension. If you’ve been paying your national insurance contributions for more than 35 years, you can claim the full state pension. You can check and see how many years you’ve been paying here, you can also top-up missing years if you need to. The full state pension will give you an annual salary of £8,767.20 or £168.60 a week. For most people, this isn’t enough to live off.

Your workplace pension should give you a top-up, but again, it’s unlikely to give you the retirement lifestyle you’re expecting. In 2018, the average workplace pension income was £166 per week[1], or £8,632 per year. Added together, a full state pension and an average workplace pension makes £17,399 annually. Experts recommend that you’ll need 80% [2]of your current income when you retire. If you’ve got a shortfall, you’ll need another source of income.

Open a Self-Invested Private Pension online in 15 minutes

Getting it sorted couldn’t be easier, you’ll have peace of mind and a brighter retirement ahead of you. Robo-advisors are a good way to get a SIPP set up quickly and hassle-free. It’s also a fab way to start the year on a high.

A Self-Invested Personal Pension (or “SIPP”) is a tax-efficient way of putting money aside for later in life. You’ll get a 25% top-up from the government, which is like free money. You’ll also be able to take out a tax-free lump sum of 25% once you hit 55 years old.

There are a lot of SIPP providers out there. Some will let you make your own investment decisions with your money, others will do it for you.

If you’d like an investment team to manage your pension pot for you, some good starting points could be:

- Nutmeg’s Personal Pension,

- True Potential Investor,

- Evestor

- Moneyfarm

- Wealth Simple

You’ll normally have to answer some questions about how you’d like your money to be managed. If you’re not sure, a good rule is to go with more equities such as stocks and shares (referred to as “more risk”) when you’ve got more than 10 years to go until you retirement. They will help to protect your money against inflation, and give it a better chance of growing than bonds or debt instruments (known as “less risky” assets).

Adding as little as £50 a month should make a difference to the kind of lifestyle you’ll be able to have when you retire. These are your golden years, it’s how your grandkids or great grandkids could remember you. It’s how you’ll live as an older person. Take a little time to organise your finances now, while you have time on your hands to get it right. It’ll take 15 minutes and you’ll have that reassurance.

This article does not constitute advice.

[1]https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/822623/pensioners-incomes-series-2017-18-report.pdf

[2] https://www.investopedia.com/retirement/retirement-income-planning/